Bernstein has downgraded Delhivery (NS:) to a Market-Perform rating and removed it from its India SMID Portfolio. The downgrade is driven by several persistent challenges that have hindered the company’s ability to stabilize its business model, according to Bernstein’s analysis.

Key Reasons for Downgrade:

1. Shrinking E-Commerce Logistics Market: Delhivery’s core business, e-commerce logistics, faces a significant challenge as major client Meesho is moving its logistics operations in-house. Meesho, which accounts for 50% of the third-party logistics (3PL) market volumes, plans to increase its internal logistics handling from 20% to 40%. This trend, seen globally among platforms like Amazon (NASDAQ:) and Coupang, poses a critical risk to Delhivery, whose revenues are heavily dependent on e-commerce logistics.

Offer: Click here to unlock powerful insights with InvestingPro! Assess stock health with over 100 parameters, get actionable ProTips, and discover the fair value of stocks—all for just INR 216/month with a 69% limited-time discount. Invest smarter and make informed decisions effortlessly!

2. Volatility and Management Challenges: Delhivery has experienced considerable volatility, with issues such as integration problems following the acquisition of Spoton and impacts from external factors like the exit of Shopee. The ongoing shifts and senior management exits suggest that the company is struggling to maintain stability.

3. Valuation Concerns: Bernstein points out that the current valuations assume high growth and strong execution, limiting further upside. To meet the target valuation, Delhivery would need to achieve an 18% revenue CAGR until FY30 with margins of 12.5%, which appears challenging given the current instability.

Investment Implications:

Earnings Estimate Revisions: Bernstein has revised its earnings estimates for Delhivery, reflecting a slower-than-expected scale-up in the e-commerce segment. EBITDA estimates for FY25-26 have been cut by 10-16%, and the target price has been adjusted from INR 520 to INR 450. The projection for achieving positive PAT has been pushed to FY27.

But investors don’t need to wait for such institutional reports to come out to decide whether to buy or sell a stock. This can be gauged simply by looking at the fair value of a stock in InvestingPro. This fair value is calculated based on several financial models and then a mean is taken to remove extreme valuations.

Image Source: InvestingPro+

As per the latest earnings, the fair value of the stock is INR 327, which is 16.1% lower than the CMP of INR 390.1. While there is a decent gap between what Bernstein thinks and InvestingPro’s valuation, both are of similar view – a decline in the upcoming performance of the company.

Image Source: InvestingPro+

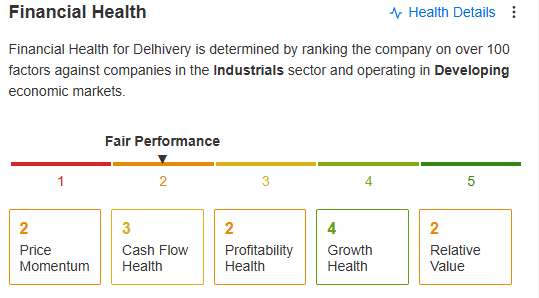

The financial health check is another good criterion to see whether the stock fundamentally qualifies to be in the portfolio or not. Here, a score of 2 out of 5 simply rejects this counter for the holding purpose.

Market Trends: The shift towards in-house logistics by e-commerce platforms is a significant global trend. In India, this shift is driven by platforms like Flipkart, Amazon, and now Meesho, which see logistics as a competitive advantage. This transition reduces the addressable market for 3PL providers like Delhivery.

Impact of Meesho’s Strategy: Meesho’s move to handle logistics internally through its arm, Valmo, is expected to impact Delhivery’s volumes. Valmo aims to lower costs and increase efficiency, which could further squeeze Delhivery’s market share.

Long-Term Outlook:

While the short-term outlook remains challenging, Bernstein notes that the long-term margin forecast of 12.5% Adjusted EBITDA is unchanged in their DCF model. However, the dependency on traditional logistics and the ongoing competition could result in a derating of the stock if these challenges persist.

Click here Subscribe to InvestingPro now at a discount of up to 69%, for just INR 216/month and unlock the full potential of your investments.

Also Read: Unveiling the Power of Fair Value with InvestingPro+

X (formerly, Twitter) – Aayush Khanna